What is the Ppf Program and How Does it Work?

The Ppf Program is an innovative solution in the realm of financial planning. It provides a structured approach to personal finance, allowing individuals to manage their savings and investments effectively. Dr. Emily Carter, a leading expert in financial strategies, once stated, “The Ppf Program can transform the way we perceive savings.” This program is designed to cater to diverse financial needs.

Many people face challenges in understanding the intricacies of the Ppf Program. It requires careful consideration of income, expenses, and future goals. Choosing the right investment options can be daunting. Each individual's financial situation is unique, which adds to the complexity. The program emphasizes long-term growth rather than quick gains, which may not appeal to everyone.

Despite its benefits, some may overlook the Ppf Program due to misconceptions or lack of awareness. It’s crucial to reflect on how we approach our finances. Many still rely on short-term solutions, missing the potential benefits of a structured program. Engaging with a credible Ppf Program can provide valuable insights and help individuals make empowered financial decisions.

What is the PPF Program?

The PPF program, or Public Provident Fund program, offers a savings scheme supported by the government. It encourages individuals to save for their retirement or future needs. The program is especially beneficial for people who want a secure and risk-free way to build funds over time.

To enroll, one needs to open an account at designated banks or post offices. Contributions are made regularly, often monthly. The interest rate is competitive, which makes it attractive for long-term savers. However, there are restrictions on withdrawals before maturity, which may not suit everyone's needs. Some may find it challenging to maintain consistent contributions due to financial fluctuations.

Over the years, the PPF program has gained popularity. Yet, not everyone understands its implications fully. Some may underestimate the importance of understanding the terms. It’s essential to recognize that while this program provides a safe haven for savings, it requires commitment and foresight. Evaluating one's financial situation before joining is crucial.

PPF Program Participation Over the Years

Key Objectives and Benefits of the PPF Program

The PPF Program, or Public Provident Fund, serves as a secure investment option. Its primary objective is to encourage long-term savings among individuals. Many people appreciate its tax benefits, which help them save money while investing. The PPF account can be opened at various financial institutions, making it accessible to many.

One key benefit of the PPF Program is the attractive interest rate it offers. This rate is typically higher than traditional savings accounts. However, the funds within the PPF account are locked for a set period. This might be a downside for some, as it limits immediate access to cash. Still, this encourages disciplined savings habits over time.

Investors often admire the low risk associated with the PPF Program. The government backs it, ensuring safety for depositors. But, this leads to a trade-off; investors may receive lower returns compared to riskier investment options. It prompts many to question if the PPF is the right choice for their financial goals. Balancing safety with growth potential remains a challenge for many savers.

What is the Ppf Program and How Does it Work? - Key Objectives and Benefits of the PPF Program

| Dimension |

Description |

Benefits |

| Interest Rate |

Typically around 7.1% per annum |

Fixed return over the investment period |

| Minimum Investment |

₹500 |

Accessible to a wide range of investors |

| Maximum Investment |

₹1.5 million |

Encourages higher savings |

| Tenure |

15 years with an option to extend |

Long-term growth potential |

| Tax Benefits |

Under Section 80C of the Income Tax Act |

Tax deduction for investments |

Eligibility Criteria for PPF Program Enrollment

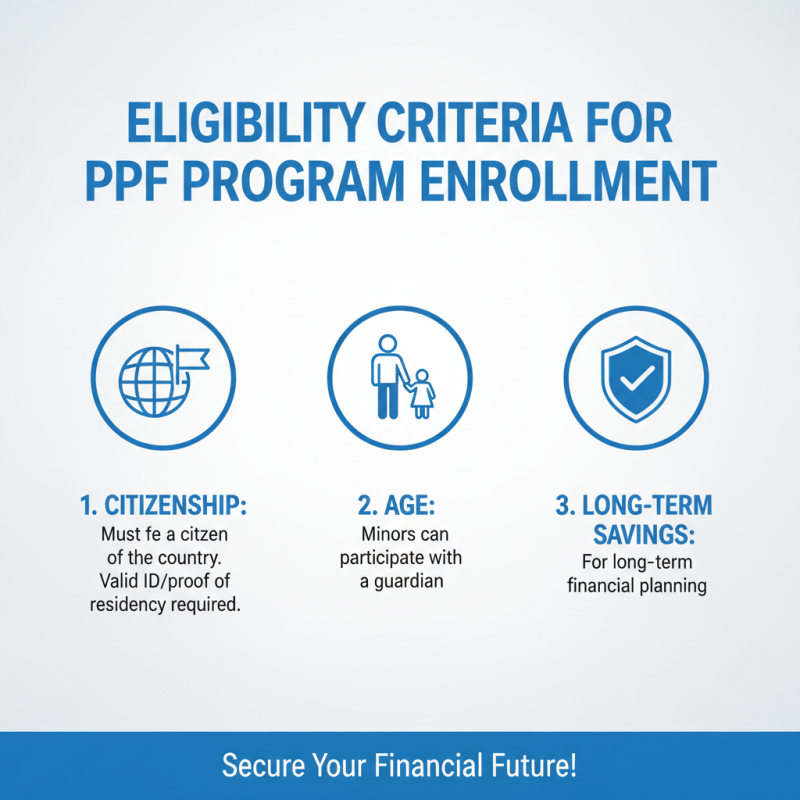

The PPF program is a valuable savings tool for long-term financial planning. To be eligible for this program, applicants must meet specific criteria. Individuals must be citizens of the country, often requiring valid documentation to prove residency. Minors can also participate with the help of a guardian, which expands the accessibility of the program.

Income levels may not play a critical role, but there are age restrictions. Participants commonly need to be adults, typically over 18 years old. Moreover, individuals wishing to enroll should not have existing accounts exceeding the permissible limit. This requirement can sometimes feel restrictive for those looking to diversify their investments.

It's important to note that some may find the application process complex. Gathering the necessary documents can be time-consuming and often leads to frustration. Doubts may arise about the terms of the program, particularly regarding interest rates or withdrawal conditions. Staying informed and seeking assistance could ease these concerns, allowing for a more streamlined experience.

How to Open a PPF Account: Step-by-Step Guide

Opening a Public Provident Fund (PPF) account is a strategic move for anyone looking to secure their financial future. This account is a long-term savings scheme backed by the government, aiming for both security and good returns. According to the latest reports, the interest rate on PPF accounts can go up to 7.1% per annum, compounded yearly. This makes it an attractive option for individuals aiming to build wealth over time.

To start a PPF account, choose a financial institution that offers this service. After selection, gather the required documents, including identity proof, address proof, and a passport-sized photograph. Fill out the application form meticulously. The minimum investment is generally low, around 500 units of currency, making it accessible to many. However, contributions can go up to 1.5 lakh units annually. Remember, this amount is locked in for 15 years.

While the benefits are clear, there are a few things to ponder. The 15-year lock-in may feel daunting for some. Accessing funds before maturity is tough, except under special circumstances. This can be a letdown for those who might need liquidity. Such constraints highlight the importance of understanding one’s financial needs before opening an account. Balancing immediate financial needs with long-term goals is crucial.

Understanding the Interest Rates and Maturity Periods in PPF

The Public Provident Fund (PPF) is a popular savings scheme. It offers attractive interest rates and tax benefits. Understanding its interest rates and maturity periods is crucial for potential investors.

Interest rates on PPF accounts are generally determined by the government. These rates tend to fluctuate quarterly. Currently, the rates are appealing, often higher than regular savings accounts. This means your money can grow significantly over 15 years.

Tip: Regular contributions can yield better returns. Aim to invest consistently each year.

PPF accounts have a maturity period of 15 years. This long-term investment can foster discipline in savings. However, some might find it tough to wait that long for returns. You can partially withdraw funds after the sixth year. This offers a bit of flexibility, but not much.

Tip: Review your financial goals often. This ensures that the PPF still aligns with your needs.

While PPF is a safe option, consider that the long lock-in can be challenging. Reflect on whether this suits your financial strategy.